“Demand Shocks in Equity Markets and Firm Responses”, with Fernando Broner, Juan Cortina, and Sergio Schmukler.

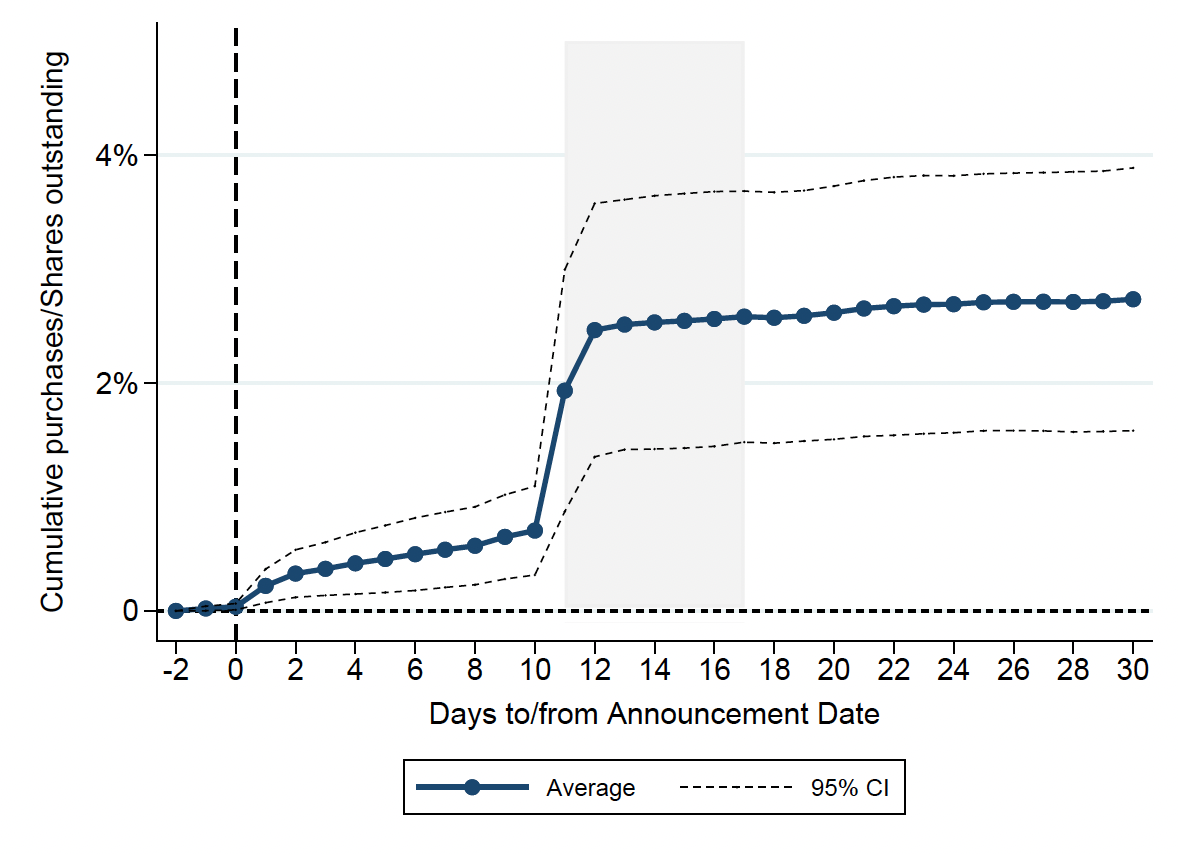

This paper examines how shifts in investor demand influence firm financing and investment decisions. For identification, the paper exploits a large-scale MSCI methodological reform that mechanically redefined the stock weights in major international equity benchmark indexes, changing the portfolio allocation of 2,508 firms across 49 countries. Because benchmark-tracking investors closely follow these indexes, the rebalancing constituted a clean shock to equity demand. The results show that portfolio rebalancing by benchmark-tracking investors generated significant capital inflows and outflows at the firm level. Firms experiencing larger inflows increased equity issuance, even more so debt financing, and real investment. The paper complements the empirical analysis with a simple model of firm financing in which a decline in the cost of equity increases the value of equity and relaxes borrowing constraints. Higher equity valuations allow firms to expand borrowing even without issuing substantial new equity, so debt financing responds more strongly than equity issuance.

“Green versus Conventional Corporate Debt: From Issuances to Emissions”, with Juan Cortina, Claudio Raddatz, and Sergio Schmukler.

This paper investigates how firms use green versus conventional debt and the associated firm- and aggregate-level environmental consequences. Employing a dataset of 127,711 global bond and syndicated loan issuances by non-financial firms across 85 countries during 2012-23, the paper documents a sharp rise in green debt issuances relative to conventional issuances since 2018. This increase is particularly pronounced among large firms with high carbon dioxide emissions. Local projections difference-in-differences estimates show that, compared to conventional debt, green bond and loan issuances are systematically followed by sustained reductions in carbon intensity (emissions over income) of up to 50 percent. These reductions correspond to as much as 15 percent of global annual emissions. Green bonds contribute to reducing emissions by providing financing to large, high-emitting firms, whose improvements in carbon intensity have significant aggregate consequences. Syndicated loans do so by channeling a larger volume of financing to a wider set of firms.

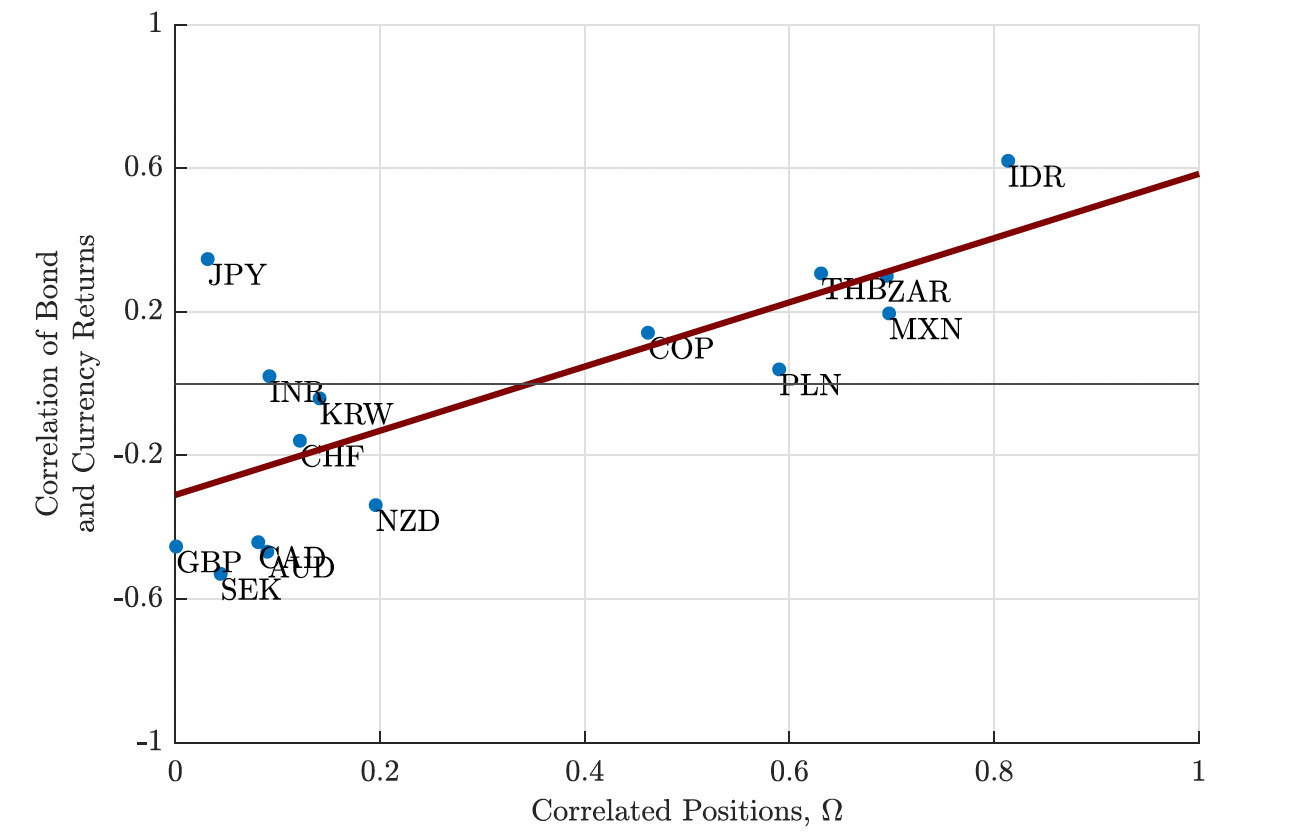

“Foreign Investors in Local-Currency Bond Markets: Implications for Bond Yields and Exchange Rates”, with Pierre De Leo, Lorena Keller, Giuliano Simoncelli, and Mauricio Villamizar Villegas.

When foreign investors acquire local-currency bonds, they must also exchange foreign for local currency. In a model with intermediation frictions, foreign inflows thus generate correlated movements in intermediaries’ bond and currency positions, and, in turn, in term and currency premia. Using data from Colombia’s bond and foreign exchange markets, we show that this mechanism accounts for key empirical patterns in intermediaries’ positions, bond yields, and exchange rates—including during inflow episodes, and in response to asset purchase policies. Consistent with the model, countries with more prevalent unhedged foreign investor flows exhibit stronger positive comovement between bond and currency returns.

“Inelastic Demand Meets Optimal Supply of Risky Sovereign Bonds”, with Matias Moretti, Lorenzo Pandolfi, Sergio Schmukler, and German Villegas-Bauer. Revise and Resubmit at Econometrica.

We study how investor demand influences government borrowing capacity, default risk, and bond prices. We develop a sovereign debt model with a rich demand structure, featuring investors with asset-allocation mandates. In our framework, bond prices depend not only on government policies and default risk, but also on investor composition and demand elasticity. We estimate this elasticity from bond price responses to the periodic rebalancing of a major emerging markets bond index, which shifts investors’ allocations. We calibrate the model using this estimate and show that a downward-sloping demand acts as a disciplining device that mitigates debt dilution by curbing future issuance. This market-based mechanism lowers default risk and allows the government to sustain higher debt. Unlike standard models, where discipline arises from default penalties, our mechanism operates through investor behavior. This distinction matters for policy: with market discipline in place, fiscal rules have milder effects on borrowing and default risk.

“Who Trades Index Rebalancings: Evidence on Benchmarking and Inelastic Demand”, with Mariana Escobar, Lorenzo Pandolfi, and Alvaro Pedraza.

Benchmark index rebalancings are widely used to study non-fundamental demand shocks, but the underlying trading is rarely observed. Exploiting transaction-level data from the Colombian stock market and additions and deletions of stocks from MSCI international equity indexes, we trace who generates benchmark-driven demand, who absorbs it, and how it affects prices. Index demand extends beyond explicit index funds and ETFs: benchmarked but nominally active foreign institutions account for most rebalancing-driven trading. Domestic investors absorb most of the shock, while arbitrage capital plays only a limited role. We show that stock demand curves are steep, especially when retail participation is larger.

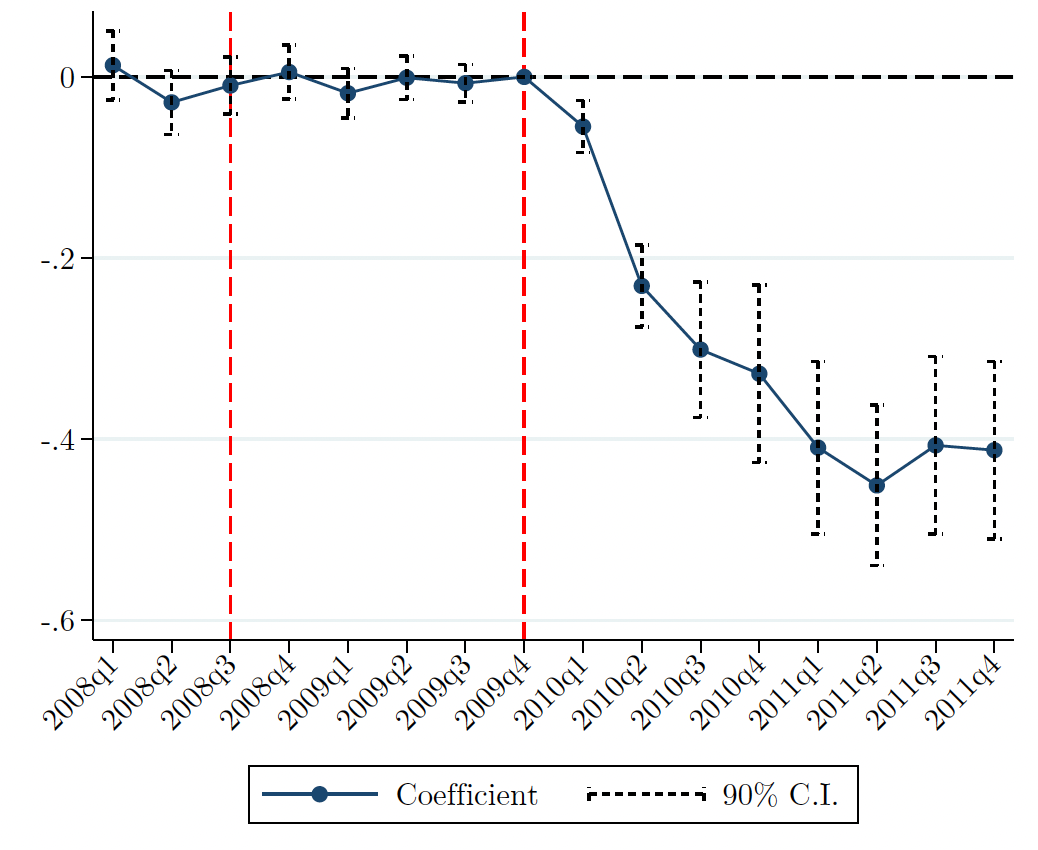

“Drug Money and Bank Lending: The Unintended Consequences of Anti-Money Laundering Policies”, with Pablo Slutzky and Mauricio Villamizar-Villegas. Conditionally accepted at the Journal of Law, Economics, and Organization.

We explore the unintended consequences of anti-money laundering (AML) policies. For identification, we exploit the implementation of the SARLAFT system in Colombia in 2008, aimed at controlling the flow of money from drug trafficking into the financial system. We find that bank deposits in municipalities with high drug trafficking activity decline after the implementation of the new AML policy. More importantly, this negative liquidity shock has consequences for credit in municipalities with little or nil drug trafficking. Banks that source their deposits from areas with high drug trafficking activity cut lending relative to banks that source their deposits from other areas. We show that this credit shortfall negatively impacted the real economy. Using a proprietary database containing data on bank-firm credit relationships, we show that small firms that rely on credit from affected banks experience a negative shock to investment, sales, size, and profitability. Additionally, we observe a reduction in employment in small firms. Our results suggest that the implementation of the AML policy had a negative effect on the real economy.